Marina Lyubimova

Marina Lyubimova

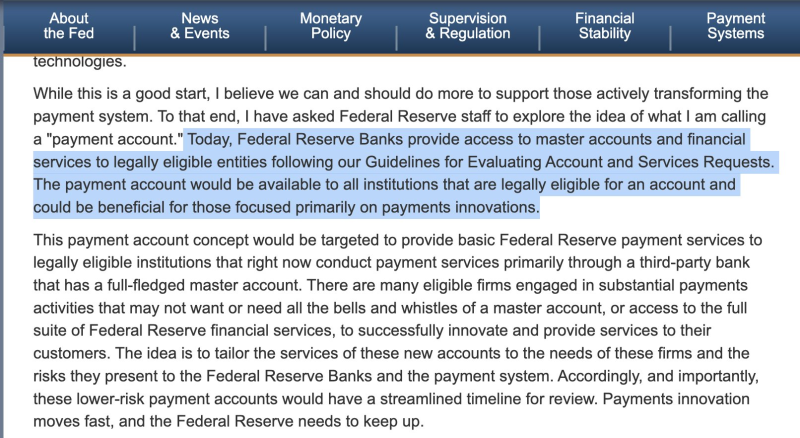

● The Federal Reserve just dropped something interesting: they're looking into creating "payment accounts" that would let fintech companies and possibly crypto firms plug directly into the Fed's payment infrastructure. It's a big deal because right now, most of these companies have to work through traditional banks to settle transactions.

● According to the Fed's statement, these accounts would be "available to all institutions that are legally eligible" and could especially help "those focused primarily on payments innovations." Basically, they're acknowledging that the financial world has changed and their systems need to catch up.

● Here's why it matters: today, if you're running a fintech app or crypto platform, you're stuck using middleman banks for settlement. That creates delays, adds costs, and limits what you can do. Direct Fed access would cut out those friction points entirely — faster transactions, better liquidity, and probably lower fees.

● But it's not all smooth sailing. Regulators are already raising eyebrows about letting non-banks into the Fed's inner circle. There are legitimate questions about cybersecurity, compliance standards, and whether digital asset platforms can handle the same regulatory scrutiny as Wells Fargo or JPMorgan. The Fed would need ironclad guardrails.

● Still, if this goes through, it could seriously shake up the payments market. More competition, lower barriers for blockchain-based solutions, and a signal that policymakers are finally ready to bring digital assets into the mainstream financial system instead of keeping them at arm's length.

Marina Lyubimova

Marina Lyubimova